How Is the Freight Market Shift Affecting Back-Office Operations?

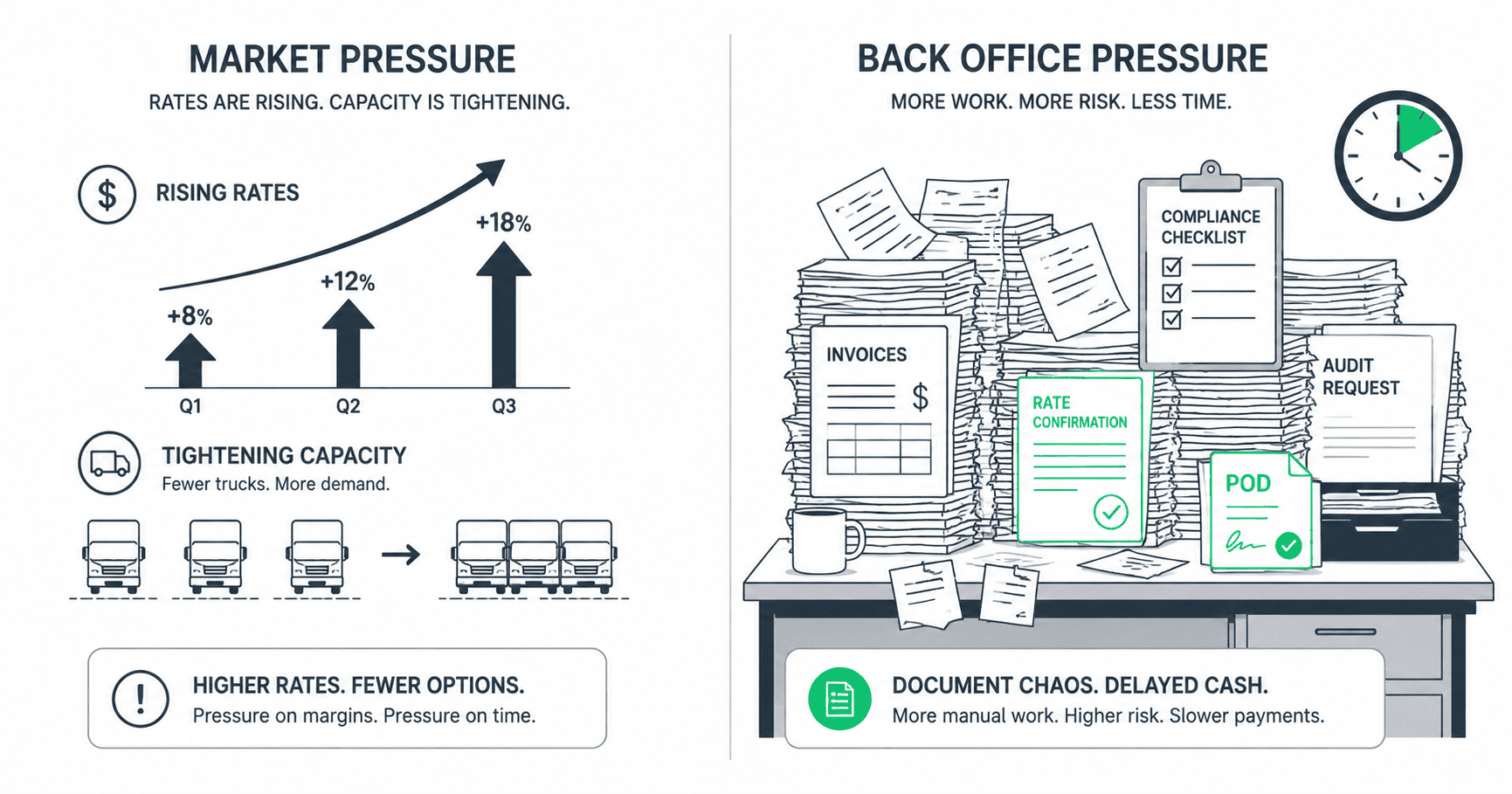

The U.S. freight market entered 2026 in a very different position than it was in a year ago. After more than three years of what many analysts called the longest freight recession in modern trucking, the cycle is turning. Capacity is tightening as carriers exit the market. Rates are climbing. Diesel prices have increased sharply. And regulatory enforcement (particularly around CDL eligibility and carrier compliance) is adding friction that further constrains the available carrier pool.

The industry conversation has focused heavily on what this means for shippers and carriers: higher transportation costs, tighter capacity, more competition for trucks. That’s the right conversation for the front office.

But there’s a back-office impact that hasn’t gotten much attention, and for freight brokerages in growth mode, it matters just as much as the rate environment.

What’s Driving the Freight Market Tightening?

The broad picture: truckload capacity is contracting through a combination of carrier exits, regulatory enforcement, and underinvestment in fleet replacement. The prolonged soft market pushed small and mid-size carriers out through margin pressure. CDL enforcement actions (particularly FMCSA‘s crackdown on non-domiciled CDLs and “CDL mills”) are removing drivers from the available pool. Diesel price increases have further compressed carrier margins, accelerating exits.

On the demand side, freight volumes are recovering gradually rather than surging. Manufacturing activity has returned to expansion territory, lean inventories are driving restocking, and import volumes are climbing. The combination of slowly recovering demand and meaningfully contracting supply is creating the conditions for sustained rate pressure through the rest of 2026 and likely into 2027.

Spot rates have already moved significantly, and contract rates are following. Industry forecasts project truckload costs running 10-17% above 2025 levels, with the potential to go higher if demand accelerates in the second half of the year.

For freight brokerages, this means the front office is getting busier and more complex. More carrier negotiations, more rate volatility, more work to cover loads at acceptable margins.

What Does Market Tightening Do to Freight Billing and Compliance?

Here’s what happens downstream when the freight market tightens.

Rate volatility creates invoice complexity. When rates are stable (as they were through much of 2023 through 2025), carrier invoice verification is relatively straightforward. The rate on the invoice matches the rate on the rate confirmation. The fuel surcharge follows a predictable formula. Exceptions are rare.

In a tightening market, rates move faster. Spot rates shift weekly. Contract rates get renegotiated mid-cycle. Fuel surcharges adjust more frequently as diesel prices climb. The result is that the rate confirmation from Monday may not match the carrier invoice that arrives Friday, not because of an error but because the rate changed between booking and billing.

Every one of those mismatches requires manual review. The carrier invoice verification process that was handling 5% exception rates during the soft market might be running at 15% or higher when rates are volatile. That’s three times the manual work on the AP side, handled by the same team.

Accessorial disputes spike during market transitions. During soft markets, carriers absorb a lot. Detention charges that technically qualify under the rate confirmation don’t get billed because the carrier wants to keep the relationship. Layover charges get waived. TONU fees get negotiated down.

When the market tightens and carriers have more options, that absorbing stops. Detention gets billed at full contract terms. Layover charges appear on invoices that didn’t have them six months ago. TONU fees go from rare to regular.

This isn’t unreasonable from the carrier’s perspective. They’re billing what the rate confirmation entitles them to. But it creates a wave of new charges flowing through the AP process, each requiring verification against the specific terms of the rate con. And on the shipper billing side, those same accessorial charges need to be billed through, which means the billing team needs to catch them before the shipper invoice goes out.

The margin on accessorial capture matters more when base rates are compressed. During the soft market, brokerages could absorb missed accessorials because the spread between carrier cost and shipper rate was wide enough. When rates tighten and margins compress, every missed accessorial charge hits the bottom line harder. A $400 detention charge that gets lost between dispatch and billing was a rounding error at 18% margin. At 12% margin, it’s a meaningful percentage of the profit on that load.

Compliance monitoring workload increases. FMCSA enforcement has intensified significantly in 2026. The crackdown on non-domiciled CDLs could affect roughly 194,000 current CDL holders as licenses come up for renewal. English Language Proficiency violations are now an out-of-service offense, over 14,000 drivers have already been placed out of service. ELD decertifications mean carriers using revoked devices face immediate shutdown at roadside inspections.

For freight brokerages, this means the carrier compliance monitoring function (verifying active authority, insurance status, safety ratings, and driver qualifications) is more critical than it’s been in years. Carriers that were compliant six months ago may not be today. The carrier compliance process needs to catch authority revocations, insurance lapses, and safety downgrades in near-real-time, not on a quarterly review cycle.

And the compliance team is usually the same team handling AP and billing. When the billing workload spikes from rate volatility and accessorial disputes, compliance monitoring is the first thing that gets deprioritized.

How Do These Pressures Compound?

Each of these pressures is manageable individually. Rate volatility adds verification work. Accessorial disputes add billing complexity. Compliance enforcement adds monitoring requirements.

Together, they compound. The back-office team that was running at 90% capacity during the soft market hits 120% when all three pressures arrive simultaneously. And in a tightening market, they arrive simultaneously, because they’re all driven by the same underlying shift in the supply-demand balance.

The compounding shows up in predictable ways. DSO starts creeping up as invoices go out slower and disputes take longer to resolve. Cash flow tightens at exactly the moment the brokerage needs cash to pay carriers faster, because in a tight market, prompt carrier payment is a competitive advantage for securing capacity. The people running the back office start triaging, which means some loads don’t get fully audited, some compliance checks don’t happen, and some accounts receivable (AR) follow-up gets pushed to next week.

None of this is dramatic. It’s gradual. But it’s the kind of gradual degradation that turns a 42-day DSO into a 56-day DSO over two quarters. By the time the trend is visible, the working capital impact is already real.

What This Means for Growing Brokerages

Brokerages that are growing into this market (adding shipper accounts, expanding lanes, increasing load counts) face a particular version of this problem. The front office is scaling to capture the opportunity. More sales reps, more dispatchers, more carrier reps. Revenue is climbing.

The back office is absorbing all the downstream complexity from that growth plus all the market-driven complexity from the tightening cycle. More loads, more rate changes, more accessorial disputes, more compliance events, more invoices, more AR follow-up, all hitting the same team.

The brokerages that navigate this well are the ones that scale back-office capacity proactively rather than waiting for DSO or cash flow to force the conversation. That might mean dedicated hires for AP or compliance. It might mean bringing in specialized teams to handle the volume. It might mean both.

The brokerages that don’t navigate it well are the ones that assume the back office will absorb the growth the way it absorbed the soft market. The soft market was forgiving: fewer exceptions, stable rates, low dispute rates. The tightening market is not.

Questions Worth Asking Right Now

If you’re running a freight brokerage heading into the second half of 2026, these are the back-office metrics worth watching:

Has your carrier invoice exception rate changed in the last 90 days? If it’s trending up, rate volatility is creating more manual work for your AP team.

Are you seeing more accessorial charges on carrier invoices than you were six months ago? If so, are those charges making it onto your shipper invoices, or are they being absorbed?

When was the last time you ran a full compliance check on every active carrier in your system? In a market where carrier exits and authority changes are accelerating, quarterly isn’t fast enough.

What’s your DSO trend line look like over the last two quarters? If it’s moving up even slightly, the back-office pressure is already showing up in your cash flow.

Is your back-office team working overtime? Triaging instead of processing? Deferring compliance monitoring to focus on billing? If yes, you’re running above capacity. The market is about to make it worse.

The freight market tightening is real, and the front-office implications are getting plenty of attention. The back-office implications deserve the same focus, because in a tight-margin, tight-capacity environment, the speed and accuracy of your billing and payment processes are a competitive advantage, not just an administrative function.

For the numbers on how these conditions actually played out, see our mid-year freight market check: volumes, rates, and what to watch through the rest of 2026.

Frequently Asked Questions

Market tightening increases rate volatility, accessorial disputes, and compliance events, all of which create more verification work, more exceptions, and more manual processing for the billing and AP teams.

During soft markets, carriers absorb charges like detention and layover to maintain broker relationships. When capacity tightens and carriers have more options, they bill at full contractual terms, creating a wave of new charges flowing through AP and AR.

When rates move frequently, the TMS auto-populated rate data goes stale faster. Rate confirmations from Monday may not match carrier invoices from Friday. Each mismatch requires manual verification, increasing the exception rate.

Scale back-office capacity proactively (through dedicated hires or outsourced teams) rather than waiting for DSO or cash flow to force the conversation. The market conditions that demand more careful billing are the same conditions that consume existing capacity.

Questions about how market conditions are affecting your back-office operations? Request a demo to see how ClearLane keeps the post-dispatch pipeline running during market transitions. Or grab the pre-billing audit checklist to evaluate your current process. Email us at info@getclearlane.com.