Why Is There a Gap Between Carrier Onboarding and Ongoing Compliance?

Most freight brokerages have a solid carrier onboarding process. Before a carrier gets approved, someone checks FMCSA authority status, verifies insurance filings, reviews safety ratings, confirms the carrier isn’t on any watch lists, and collects the necessary documentation: W-9, COI, signed carrier agreement.

The problem isn’t at onboarding. It’s everything that happens after.

Carrier compliance isn’t static. FMCSA authority can be revoked. Insurance policies can lapse or be cancelled without the broker being notified. Safety ratings can change after an audit or a pattern of roadside violations. A carrier that was fully compliant when they were onboarded six months ago may not be compliant today.

The question every freight brokerage should be able to answer is whether every carrier in their active database is fully compliant right now. Not at the time they were approved. Right now.

What Does Carrier Compliance Actually Mean for Freight Brokers?

Carrier compliance for freight brokerages covers several areas, each with its own data sources and monitoring requirements.

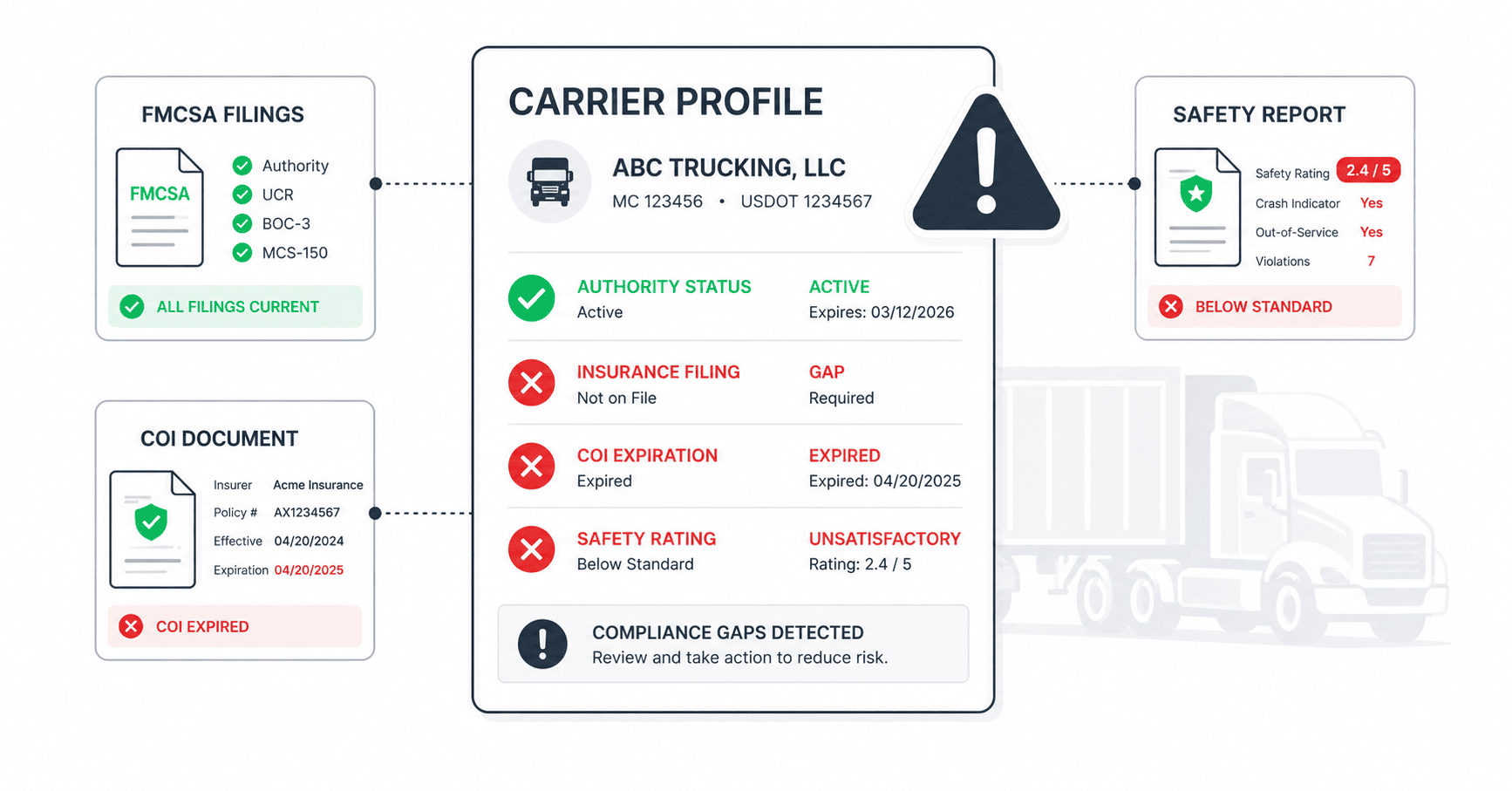

FMCSA operating authority is the baseline. A carrier must have active authority to operate legally. Authority can be revoked for a range of reasons: safety violations, insurance filing failures, failure to update registration information, or enforcement actions. When authority is revoked, any loads tendered to that carrier are being moved by an entity that isn’t legally authorized to operate as a motor carrier. The liability implications for the brokerage are significant.

Insurance is the most common compliance gap. Carriers are required to maintain minimum insurance levels: $750,000 in public liability for general freight, $1,000,000 for certain commodity types, plus cargo insurance as required by broker-carrier agreements. Insurance filings with FMCSA (BMC-91 or BMC-34) are the official record of coverage. But insurance cancellations don’t always show up immediately in FMCSA systems, and the lag between a policy lapsing and the FMCSA database reflecting that lapse can create a window where a broker is tendering loads to an uninsured carrier without knowing it.

COI (Certificate of Insurance) tracking adds another layer. The COI the carrier provided at onboarding has an expiration date. When that date passes, the carrier needs to provide an updated COI. At many brokerages, nobody is tracking those expiration dates systematically. The COI sits in a file, and unless someone pulls it up, the expiration passes unnoticed.

Safety ratings and inspection data provide a picture of the carrier’s operational safety. FMCSA’s BASIC scores track performance across categories like unsafe driving, crash indicators, hours of service compliance, vehicle maintenance, and driver fitness. A carrier whose scores have deteriorated since onboarding represents higher risk, both safety risk and liability risk in the event of an incident.

And the compliance landscape has gotten more complex. FMCSA’s crackdown on non-domiciled CDLs means carriers employing drivers with affected licenses may face sudden workforce disruptions, and the compliance responsibility flows upstream to the broker who tendered the load. English Language Proficiency is now an out-of-service offense, meaning drivers who can’t demonstrate English proficiency during an inspection can be shut down on the spot. ELD decertifications have placed carriers using revoked devices at risk of roadside out-of-service orders.

Each of these changes creates a compliance event that didn’t exist a year ago. The carrier that was fully compliant at onboarding may now have drivers with questionable CDL status, non-compliant ELDs, or insurance gaps that appeared after their COI was last verified.

Why Does Carrier Compliance Monitoring Break Down at Growing Brokerages?

The data to monitor all of this exists. FMCSA’s SAFER system, the Clearinghouse, insurance verification databases, and carrier monitoring services all provide access to the information a broker needs to assess carrier compliance on an ongoing basis.

The breakdown isn’t in data availability. It’s in who’s responsible for checking it and how often.

At most growing freight brokerages, carrier compliance monitoring sits with the same team that handles carrier invoice verification, shipper billing, POD retrieval, and AR follow-up. Compliance monitoring is important, but it’s not urgent in the way that a past-due invoice or a missing POD is urgent. It doesn’t have a customer calling about it. It doesn’t have a deadline attached to it.

So it gets deprioritized. The team does compliance checks at onboarding, does a periodic review when someone remembers or when a shipper requests documentation, and otherwise relies on the assumption that nothing has changed.

That assumption deserves a closer look. Insurance lapses happen quietly. Authority changes happen without notice. Safety scores shift after inspections that the broker never sees. And in a market where carrier exits are accelerating, the pace of compliance changes is faster than it was during the stable years.

The risk isn’t theoretical. When a broker tenders a load to a carrier with lapsed insurance and that carrier is involved in an accident, the broker’s liability exposure is real. The shipper’s contract with the broker typically requires the broker to use compliant carriers. If the broker can’t demonstrate that they verified compliance at the time of tendering, the liability argument writes itself.

What Does Systematic Carrier Compliance Monitoring Look Like?

Closing the compliance gap requires moving from periodic checks to systematic monitoring. The key elements are straightforward, but they require dedicated capacity. That is why this function, like AP audit and POD retrieval, often ends up being the work that justifies bringing in a specialized team.

Authority status monitoring should be automated or checked at defined intervals: daily or weekly, not quarterly. When a carrier’s authority status changes, that change should trigger an alert and an immediate hold on new load tenders until the status is resolved.

Insurance verification should happen against FMCSA filing data, not just the COI on file. COIs reflect what the carrier provided at a point in time. FMCSA filings reflect what the insurance company has reported. If there’s a gap between the two, the FMCSA data is the more reliable indicator.

COI expiration tracking should be systematic. Every COI in the carrier database has an expiration date. A 30-day advance notification to the carrier requesting an updated COI, followed by a 15-day reminder, followed by a hold on tendering if the updated COI isn’t received by expiration. That’s the process. It’s simple to design and tedious to execute across hundreds of active carriers.

Safety data review should happen on a regular cadence. Not every carrier needs a deep dive every month, but carriers with deteriorating BASIC scores, recent roadside violations, or patterns of poor performance need to be flagged and reviewed. The standard should be clear: above a defined threshold, the carrier gets restricted or removed from active status until the issue is resolved.

All of this should produce a compliance report that answers the question: which carriers are fully compliant, which have open issues, and which are on hold? The report should be current, not a snapshot from last quarter.

The Cost of Getting It Wrong

The financial exposure from compliance gaps isn’t limited to catastrophic events like accidents involving uninsured carriers. There are several layers of cost.

Shipper audits are increasingly common. Large shippers and enterprise customers audit their freight providers’ carrier compliance programs as part of vendor management. A broker that can’t demonstrate systematic compliance monitoring risks losing the account, not because of a specific incident but because the compliance documentation isn’t there.

Insurance costs for the brokerage itself are affected by carrier quality. Brokerage E&O (errors and omissions) and contingent liability insurance premiums are influenced by the broker’s risk management practices. Demonstrating systematic carrier compliance monitoring can support better insurance terms. The absence of it can drive premiums higher.

Operational disruption from mid-shipment compliance failures is costly and hard to quantify. A carrier gets pulled over and placed out of service because of an ELD violation or a CDL issue. The load is stranded. The broker has to find a replacement carrier, manage the customer communication, and eat the cost of the recovery. That cost is real and it’s avoidable with upstream monitoring.

And the reputational risk of being associated with a non-compliant carrier in a serious incident is the kind of damage that doesn’t show up on a spreadsheet but can affect the business for years.

Connecting Compliance to the Full Pipeline

Carrier compliance monitoring isn’t a standalone function. It connects directly to the broader post-dispatch pipeline.

On the AP side, carrier compliance verification should be part of the invoice approval process. Before a carrier invoice gets approved for payment, the carrier’s compliance status should be confirmed. Paying a carrier whose authority has been revoked creates a paper trail that no broker wants to explain.

On the shipper billing side, compliance documentation often needs to accompany the invoice, particularly for enterprise shippers who require proof that compliant carriers were used. Having that documentation ready at billing time, rather than scrambling to produce it during a shipper audit, saves time and protects the relationship.

And for carrier relationship management, compliance data should feed into the ongoing evaluation of which carriers get preferred status and which get restricted. A carrier with strong compliance history and clean safety data deserves a different level of access than one with recurring issues.

ClearLane’s carrier compliance monitoring covers authority verification, insurance filing checks, COI tracking, and safety data review as part of the full post-dispatch pipeline. It’s the same team handling AP audit, shipper billing, and AR, which means compliance isn’t siloed from the operational workflows that depend on it.

Starting Points

If you’re running a freight brokerage and want to assess your current compliance monitoring, start with these:

Pull a list of every carrier you’ve tendered a load to in the last 90 days. Check their FMCSA authority status and insurance filings right now. How many have a status that’s changed since onboarding?

Review your COI files. How many have expired? How many carriers on your active list have a COI that’s more than 12 months old?

Check your process for ongoing monitoring. Is it documented? Is it assigned to a specific person? Does it run on a defined schedule, or does it happen when someone remembers?

If any of those answers make you uncomfortable, the gap is real. It’s worth closing before the market makes it more expensive.

The carrier compliance template on the ClearLane site is a starting point for building or evaluating your monitoring process.

Frequently Asked Questions

Carrier compliance monitoring is the ongoing process of verifying that every carrier in a broker’s active database maintains valid FMCSA operating authority, current insurance filings, up-to-date COI documentation, and acceptable safety ratings, not just at onboarding but continuously.

Authority status and insurance filings should be checked weekly or daily, not quarterly. COI expiration tracking should be systematic with 30-day advance notifications. Safety data should be reviewed on a regular cadence with defined thresholds for flagging deterioration.

The broker faces liability exposure if the carrier is involved in an incident. Shipper contracts typically require the use of compliant carriers, so the broker may also face contract violations, lost accounts, and increased E&O insurance premiums.

A COI is what the carrier provides. It reflects coverage at a point in time. FMCSA filings (BMC-91, BMC-34) reflect what the insurance company has reported. The FMCSA filing is the more reliable indicator because it’s updated by the insurer, not the carrier.

Compliance monitoring is important but not urgent. It gets deprioritized when the back-office team is busy with billing, AR, and POD retrieval. A dedicated team provides the consistency that shared teams can’t maintain, checking every carrier on a defined schedule.

Questions about your carrier compliance process? Request a demo to see how ClearLane handles ongoing compliance monitoring for freight companies. Or email us at [email protected].