How Are Rising Insurance Costs Affecting Trucking Carriers?

Commercial trucking insurance has been getting more expensive for years, and the trend is accelerating. According to ATRI, insurance averaged 10.2 cents per mile in 2024, marking the fifth consecutive year of increases. Insurance cost and availability now ranks as the third most critical issue facing the trucking industry, up one spot from the prior year.

Carriers absorbing these premium increases feel it in cash flow first, which puts pressure on how fast they invoice and how well they collect. That is the case for billing and collections support built for trucking companies.

The drivers behind the cost increases are well-documented: nuclear verdicts (jury awards exceeding $10 million) surged 52% in 2024. Vehicle repair and replacement costs continue to climb. Litigation costs have increased across the industry. And the number of insurers serving the trucking market is shrinking, and those that remain are writing fewer policies and being more selective about which risks they accept.

For carriers, the impact is direct: higher premiums, stricter underwriting standards, and fewer coverage options. New-authority carriers typically pay 40 to 100% more than established carriers, and some find it difficult to secure coverage at all. Even established fleets are facing renewal increases that strain operating margins.

This is primarily discussed as a carrier problem: an operating cost issue that affects profitability and, at the margins, pushes some carriers out of the market. That framing is accurate but incomplete. For freight brokerages that rely on those carriers to move freight, rising insurance costs create a compliance monitoring challenge that directly affects risk exposure.

Why Should Freight Brokers Care About Carrier Insurance Costs?

Rising insurance costs affect broker compliance in several specific ways that go beyond the headline cost numbers.

Coverage changes happen more frequently in expensive markets. When insurance premiums jump at renewal, carriers make decisions. Some absorb the increase. Some shop for a new insurer and switch policies, which creates a transition period where the old policy is cancelled and the new policy is being filed with FMCSA. Some reduce their coverage limits to manage costs. And some let coverage lapse, even briefly, while they negotiate new terms.

Each of these events changes the carrier’s compliance status in ways that may not be immediately visible to the broker. FMCSA insurance filing databases (BMC-91 and BMC-34) reflect what the insurance company has reported, but there can be a lag between a policy cancellation and the database update. A broker checking FMCSA records might see active coverage when the actual policy has already lapsed.

Carrier-provided COIs become less reliable as a standalone verification source. The Certificate of Insurance a carrier provided at onboarding reflects coverage at a specific point in time. In a stable insurance market, that coverage is likely to remain in place until the policy expiration date shown on the COI. In a volatile insurance market, mid-term cancellations, insurer changes, and coverage modifications happen more frequently. The COI on file may not reflect current coverage.

The carrier pool that’s most available may also be the most compliance-vulnerable. In tight freight markets, the carriers with available capacity are often smaller operators and newer authorities, exactly the segments facing the highest insurance cost pressure. These carriers are valuable to brokerages that need coverage, but they’re also the ones most likely to have compliance gaps related to insurance.

Shipper requirements for carrier insurance are tightening. Large shippers are increasingly specifying minimum insurance requirements for carriers used by their freight providers, and auditing compliance with those requirements. A shipper that requires $1 million in liability coverage expects that every carrier used on their freight meets that threshold. If a broker’s compliance monitoring can’t demonstrate that verification, the shipper relationship is at risk.

How Should Broker Compliance Monitoring Change in a Rising Insurance Market?

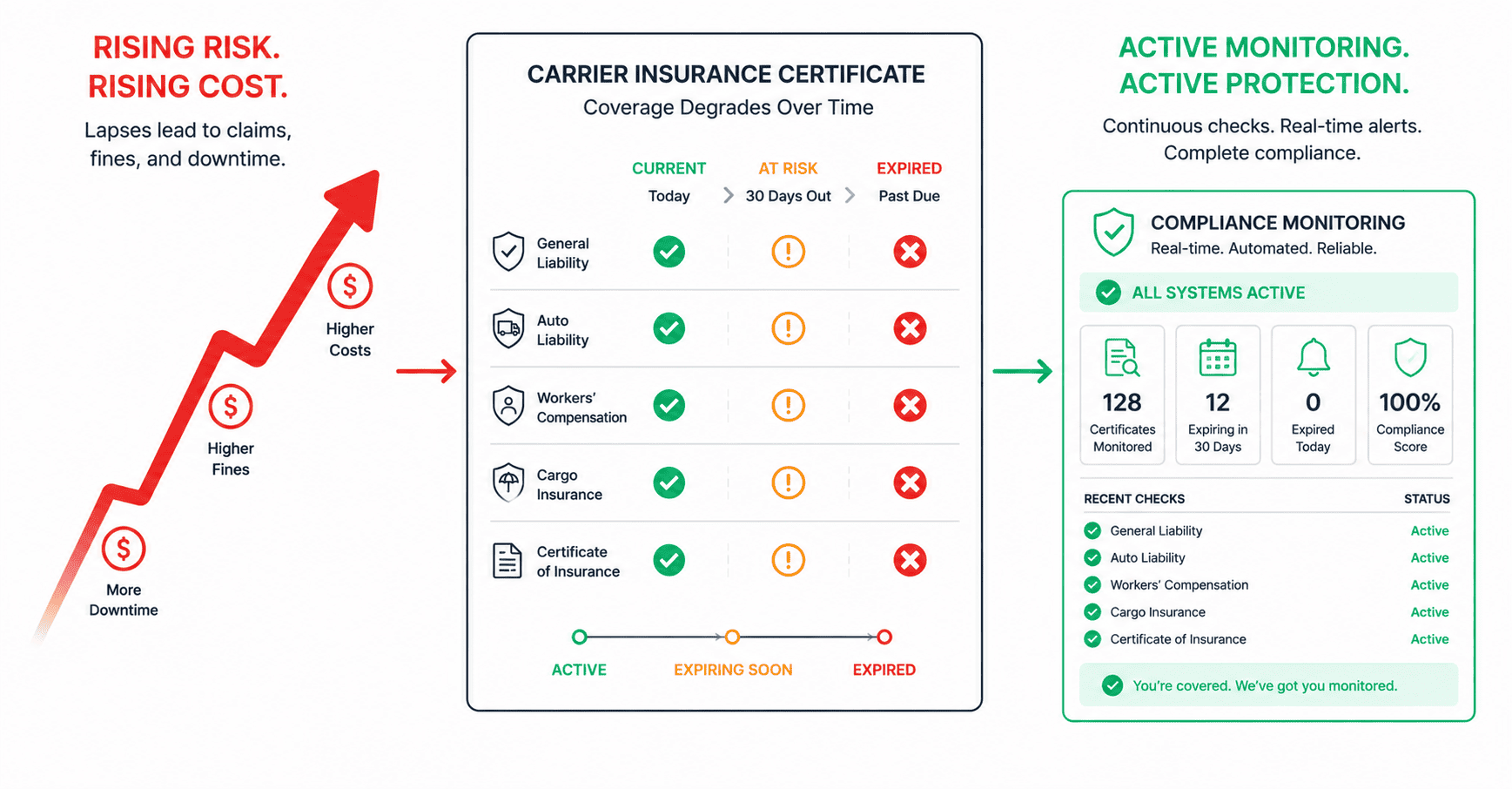

The rising insurance cost environment doesn’t change what compliance monitoring should check. It changes how frequently it needs to check and how much reliance can be placed on static documents like COIs.

Insurance filing verification should be ongoing, not one-time. Checking a carrier’s FMCSA insurance filings at onboarding establishes a baseline. Checking again monthly (or more frequently for carriers with recent authority or a history of coverage changes) catches lapses that develop between onboarding and the next load tender.

COI expiration tracking should be systematic and proactive. Every COI has an expiration date. A process that sends a renewal request to the carrier 30 days before expiration, followed by a 15-day reminder, followed by a tender hold if the updated COI isn’t received by expiration: this should be the standard. In practice, most brokerages don’t track COI expirations systematically.

Cross-referencing between the COI on file and FMCSA filings adds a verification layer. If the COI shows a policy with Insurer A and the FMCSA filing shows Insurer B, that discrepancy needs investigation. It may reflect a mid-term insurer change that the carrier didn’t communicate. It may be a timing issue with filing updates. Either way, it’s a data point that requires attention.

New-authority and small-fleet carriers deserve additional monitoring frequency. These segments face the highest insurance cost pressure and the most limited options. A small carrier that had coverage through a specialty insurer may find that insurer exited the market at renewal. The replacement coverage, if they find it, may have different terms, different limits, or a gap between the old policy’s cancellation and the new policy’s effective date.

The Connection to Carrier Payment and Operations

Insurance compliance affects more than just risk management. It connects to several operational functions.

Carrier payment timing matters in the insurance context. Carriers struggling with insurance costs are also likely struggling with cash flow. Prompt carrier payment from the broker doesn’t just maintain the relationship. It helps the carrier maintain the financial stability that supports continued insurance coverage. A carrier that’s consistently waiting 45 days for broker payment has less cash available to cover a $15,000 quarterly insurance premium.

Load tendering decisions should include compliance status. Before a load is tendered to a carrier, the carrier’s current compliance status, including insurance, should be verified. In a manual process, this means someone checks before assigning the load. In an automated or semi-automated process, the TMS or compliance platform flags carriers with open compliance issues before a load can be tendered.

Claims handling is more complex when insurance coverage is in question. If a carrier is involved in an incident and their insurance coverage is disputed (because the policy lapsed, the limits were reduced, or the filing doesn’t match the COI), the claims process becomes significantly more complicated for the broker. The broker’s contingent cargo insurance or errors and omissions policy may be implicated. The investigation into coverage status at the time of the incident consumes staff time and creates uncertainty.

What to Do

For freight brokerages, the rising insurance cost environment creates a clear action item: tighten the frequency and rigor of insurance compliance monitoring.

Review your monitoring frequency. If you’re checking carrier insurance status only at onboarding, increase to monthly verification against FMCSA filings for all active carriers, and weekly for new-authority or small-fleet carriers.

Implement COI expiration tracking with automated reminders. Don’t wait for carriers to proactively send updated COIs. Most won’t. A defined request-reminder-hold process ensures coverage gaps are identified before loads are tendered.

Cross-reference COIs against FMCSA filings. Discrepancies between the two are not necessarily problems, but they always warrant investigation.

Define what happens when a compliance gap is identified. A carrier with a lapsed insurance filing should be immediately restricted from new tenders until the filing is current. The policy should be clear, documented, and consistently applied.

The carrier compliance template on the ClearLane site includes insurance verification as one of the standard monitoring checks. ClearLane’s compliance monitoring tracks insurance filings, COI expirations, and FMCSA filing status as part of the full post-dispatch pipeline.

Frequently Asked Questions

When premiums climb, carriers face harder choices: some downgrade coverage, switch insurers (creating transition gaps), reduce limits, or let policies lapse temporarily. Each change affects the carrier’s compliance status in ways that may not be immediately visible to the broker.

Monthly verification against FMCSA filings for all active carriers, with weekly checks for new-authority or small-fleet carriers who face the highest insurance cost pressure.

A COI reflects what the carrier provided at a point in time. FMCSA filings reflect what the insurance company has reported. In a volatile insurance market, mid-term cancellations and insurer changes happen more frequently, making COIs alone less reliable.

Smaller carriers and owner-operators face the highest premium pressure. Some exit the market, some reduce coverage. The carriers most available in tight-capacity periods may also be the ones most vulnerable to insurance gaps.

Questions about your insurance compliance monitoring? Request a demo to see how ClearLane handles carrier compliance in the current insurance environment. Or email us at info@getclearlane.com.